For many retirees, staying active in the workforce is about more than financial necessity. Part-time work provides purpose, social connection, and an opportunity to supplement retirement income without relying solely on savings. Recognising this, the Australian government introduced the Work Bonus — a program designed to reward pensioners who choose to keep working.

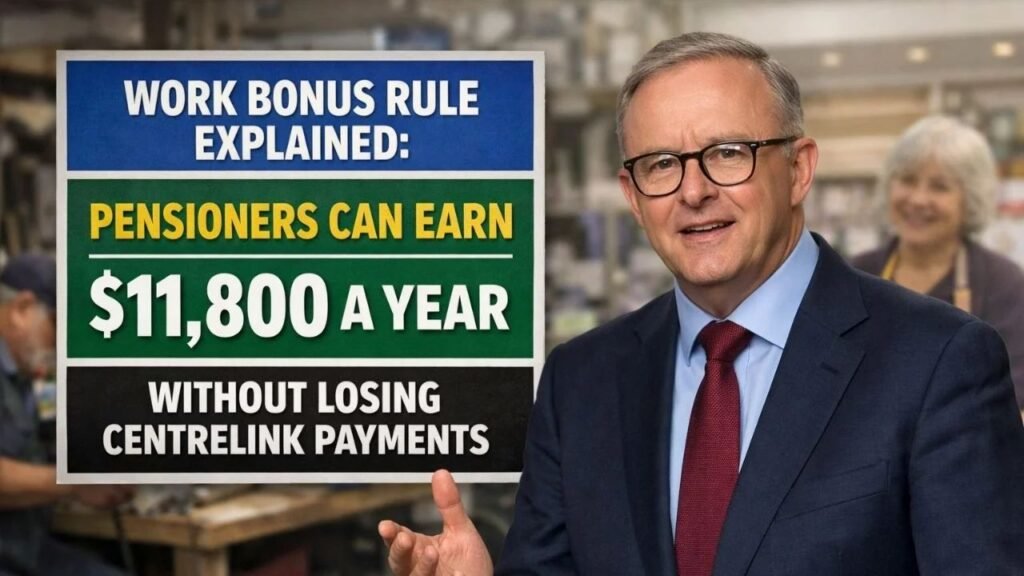

In 2026, the Work Bonus continues to play a vital role in retirement income planning. Eligible pensioners may earn up to $11,800 per year in employment income without immediately affecting their Age Pension payments. Understanding how this rule works can help retirees make confident decisions about working during retirement.

What the Work Bonus Is and Why It Exists

The Work Bonus is a feature within the Age Pension income test that reduces the amount of employment income counted when calculating pension payments.

In simple terms, it allows pensioners to earn money from work while still receiving their pension, up to certain limits.

The program was created with two main goals:

- Encourage older Australians to remain in the workforce

- Provide financial flexibility during retirement

- Support industries experiencing labour shortages

- Promote healthier, more active retirement lifestyles

Rather than discouraging work, the Work Bonus acknowledges that retirement today often includes flexible work arrangements.

How the Work Bonus Works in 2026

Under the current rules, the first $300 of employment income per fortnight is excluded from the Age Pension income test.

This means that income up to this amount does not reduce pension payments.

Annual Work Bonus Potential

When calculated across the year, this fortnightly allowance adds up to approximately $11,800 annually in exempt employment income.

This provides retirees with a meaningful opportunity to earn extra money without risking immediate reductions to their pension.

Accumulating Unused Work Bonus Credits

One of the most valuable features of the Work Bonus is the ability to accumulate unused credits.

If a pensioner does not work for a period of time, the unused $300 fortnightly exemption builds up in a Work Bonus balance. This balance can later be used to offset higher earnings in future fortnights.

For example:

- If no work income is earned, the $300 credit accumulates

- Over time, these credits create flexibility

- Higher income in later periods may still be partially exempt

This accumulation system supports seasonal or irregular work patterns.

Types of Work That Qualify

Not all income is treated equally under the Work Bonus. The scheme applies specifically to employment income.

Eligible Income Sources

Work Bonus applies to:

- Casual employment

- Part-time work

- Short-term contract roles

- Seasonal work

- Self-employment income (in some cases)

These flexible work types are common among retirees who want to remain engaged without committing to full-time hours.

Income That Does Not Qualify

Certain income sources are not eligible under the Work Bonus.

These include:

- Investment income

- Rental property income

- Dividends from shares

- Interest from savings

- Capital gains

These types of earnings are still assessed under standard income test rules.

How Pensioners Benefit Financially

The Work Bonus provides multiple financial advantages beyond simple income flexibility.

Increased Disposable Income

The most obvious benefit is the ability to earn extra money without losing pension payments immediately.

This additional income can help retirees cover:

- Rising living costs

- Healthcare expenses

- Travel and leisure activities

- Home maintenance

- Unexpected financial needs

With inflation continuing to affect household budgets, this flexibility has become increasingly valuable.

Extended Financial Independence

By supplementing pension income with work earnings, retirees may preserve personal savings for longer.

This approach reduces pressure on retirement funds and supports long-term financial security.

Real-World Example of Work Bonus Impact

Understanding how the Work Bonus applies in practice helps clarify its value.

Consider the following scenario:

Example Income Calculation

If a pensioner earns $300 per fortnight, none of this amount is counted under the income test.

If the pensioner earns $500 per fortnight, only $200 is counted toward the income test after the $300 Work Bonus exclusion.

This structure ensures that working modest hours does not immediately reduce pension payments.

For retirees considering flexible employment, this rule can make part-time work financially worthwhile.

Work Bonus Benefits for Couples

Couples receiving the Age Pension may also benefit from the Work Bonus.

Each eligible partner receives their own Work Bonus allowance.

This means:

- Both partners can earn income

- Each partner receives the $300 fortnightly exemption

- Household income flexibility increases

For couples exploring part-time work opportunities, this dual eligibility can significantly improve financial outcomes.

Lifestyle Advantages Beyond Financial Gains

While the financial benefits are substantial, the Work Bonus also supports broader lifestyle goals.

Staying Mentally and Physically Active

Continuing to work — even casually — promotes mental engagement and physical movement.

Many retirees report improved wellbeing when participating in part-time employment or community-based work.

Social Connection and Purpose

Work environments offer valuable social interaction, which can reduce feelings of isolation during retirement.

Maintaining professional relationships and daily routines often contributes to improved quality of life.

Flexible Work Opportunities

Modern work environments increasingly support flexible schedules, making it easier for retirees to balance personal interests with paid work.

Common roles for retirees include:

- Customer service positions

- Administrative support

- Retail assistance

- Consulting roles

- Mentoring or training positions

These flexible arrangements make workforce participation more accessible than ever.

Reporting Requirements for Pensioners

Although the Work Bonus provides income flexibility, pensioners must still meet reporting requirements.

Reporting Employment Income

All employment income must be reported accurately and on time.

Required reporting typically includes:

- Gross income earned

- Hours worked

- Employer details

- Self-employment earnings (if applicable)

Failure to report income correctly may result in overpayments or compliance issues.

Maintaining accurate records helps ensure smooth pension management.

Policy Updates and Future Changes

Like many government programs, the Work Bonus may be adjusted over time.

Changes may occur due to:

- Economic conditions

- Labour market trends

- Cost-of-living adjustments

- Government policy reforms

Staying informed about rule changes allows pensioners to adapt their work plans accordingly.

Regularly reviewing pension statements and official communications helps ensure compliance with current rules.

Strategic Planning for Working During Retirement

For retirees considering part-time work, planning ahead can maximise the benefits of the Work Bonus.

Consider Flexible Employment Options

Look for roles that allow adaptable working hours. This supports gradual transitions between work and retirement.

Flexible employment also makes it easier to manage income within Work Bonus limits.

Track Work Bonus Balances

Monitoring accumulated Work Bonus credits provides greater control over earning patterns.

This is especially useful for seasonal or project-based work arrangements.

Seek Professional Financial Advice

Financial professionals can help retirees structure income in ways that optimise pension outcomes.

Advice may include:

- Income timing strategies

- Work schedule planning

- Asset and income balancing

- Tax considerations

Professional guidance can help retirees make the most of available benefits.

The Bigger Picture: Retirement in a Modern Workforce

Retirement today looks very different from previous generations. Many retirees choose to remain active, productive, and financially engaged.

The Work Bonus reflects this shift by supporting flexible employment during retirement years.

Rather than forcing retirees to choose between work and pension income, the program creates opportunities to combine both — strengthening financial security and personal wellbeing.

Final Thoughts: Making the Most of the Work Bonus in 2026

The Work Bonus remains one of the most valuable tools available to pensioners who want to supplement their income without sacrificing their Age Pension.

With the ability to earn up to $11,800 per year under current rules, retirees can enjoy greater financial freedom while staying engaged in meaningful work.

By understanding how the Work Bonus operates — and planning income carefully — pensioners can create a retirement lifestyle that balances flexibility, stability, and independence.

For many retirees, the future of retirement is not about stepping away from work entirely, but about working smarter, staying connected, and building a lifestyle that supports both financial security and personal fulfilment.